Monopolistic Competition

- A large number of firms compete

- Each firm produces a differentiated product

- Firms compete on product quality, price and marketing

- Firms are free to enter and exit the industry

Product Differentiation

- When the firm makes a product that is slightly different from the products of competing firms

Entry and Exit

- There are no barriers to entry

- Firm cannot make an economic profit in the long run

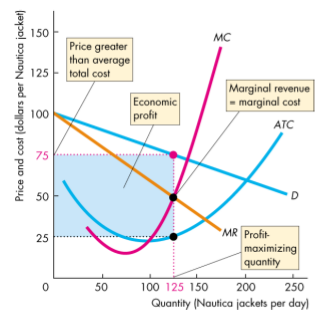

Price and Output

- The firm in monopolistic competition operates like a single-price monopoly

- The firm produces the quantity at which MR=MC and sells that quantity for the highest possible price

- It makes an economic profit when P>ATC

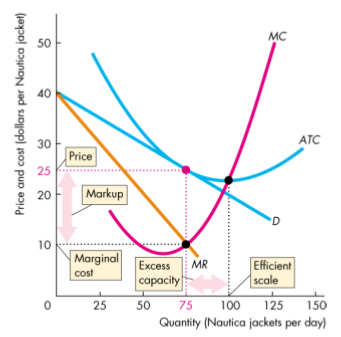

- Long run economic profit =0,P=ATC

Compared to Perfect Competition

- Excess capacity - if a firm produces less than the quantity at which ATC is a minimum

- Markup - the amount by which its price exceeds its marginal cost

- Firms operate with excess capcity in long-run equilibrium

- Produce less than the efficient scale - the quantity at which ATC is a minimum

- Doward sloping demand curve

- Firms operate with positive markup

- Result of the downward sloping demand curve

- Firms in perfect competition have no exccess capacity and no markup

- Result of the perfectly elastic demand curve

Product Development and Marketing

- Firms must continously innovate and develop new products

- New firms enter similar products compete away economic profits

Advertising

- Increase costs

- Signal quality - send a message to uninformed people

- Create perception of product differentiation even when th actual product differences are small