Output and Costs

Short-Run Cost

- To produce more output in the short run, the firm must employ more labour, which means that it must increase its costs

Total cost (TC)

- The cost of all resources used

Total fixed cost (TF)

- The cost of the firm's fixed inputs

- Do not change with output

Total variable cost (TVC)

- The cost of the firm's variable inputs

- Change with the outout

Relationship:

Total cost curves

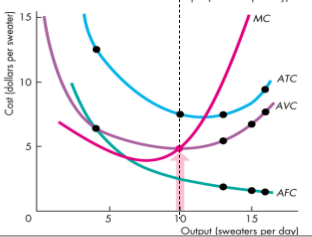

Marginal Cost (MC)

- The increase in total cost that results from a one-unit increase in total product

- Increasing marginal returns => marginal cost falls as output increases

- diminishing marginal returns => marginal cost rises as output increases

Average fixed cost (ACF)

- Total fixed cost per unit of output

Average variable cost (AVC)

- Total variable cost per unit of output

Average total cost (ATC)

- Total cost per unit of output

Relationship:

Cost Curves and Product Curves

- The shape of a firm's cost curves are determined by the technology it uses

- By the shape of the total product curve

- MC _is at its minimum at the same output level at which _MP is at its maximum

- When MP is rising, MC is falling

- AVC is at its minimum at the same output level at which AP is at its maximum

When AP is rising, AVC is falling

The AVC curve is U-shaped because

- Initially MP exceeds AP, which brings rising AP and falling AVC

- Eventually MP falls below AP, which brings falling AP and AVC

The ATC curve is U-shaped for the same reasons

- The ATC falls at low output levels because AFC is falling quickly

- ATC curve is the vertical sum of the AFC curve and the AVC curve

- Influence of two opssing forces

- Spreading total fixed cost over a larger output - AFC curve slopes downward as output increases

- Eventually diminishing returns - the AVC curve slopes upwards and AVC increases more quickly than AFC is decreasing

Shifts in the cost curves

- The position of a firm's cost cruves depend on techonlogy and prices of factors of production

Technology

- Influences both the product curves and the cost curves

- Increase in productivity shifts the product curves upward and the cost curves downward

- If the technological advance results in the firm using more capital and less labour, fixed costs increase and variable cost decrease

- Average total cost increase at low output levels and decreases at output levels

Prices

- Increase in the price of a factor of production increases costs and shifts the cost curves

- Increase in a fixed cost shifts the TC and ATC upwards but does not shift the MC curve

- Increase in a variable cost shifts the TC, ATC, and MC curves upward

Long-Run Cost

- All inputs are variable and all costs are variable

- Depends upon on the firm's product function - the relationship between the maximum output attainable and the quantitiesof both capital and labour

Diminishing Marginal Product of Capital

Marginal product of capital - the increase in output resulting from a one-unit increase in the amount of capital employed, holding constant the amount of labour employed

- A firm's production function exhibits diminishing marginal returns to labour (for a given plant) and diminishing marginal returns to capital (for a quantity of labour)

- Creates a set of short run, U-shaped cost curves for MC, AVC, and ATC

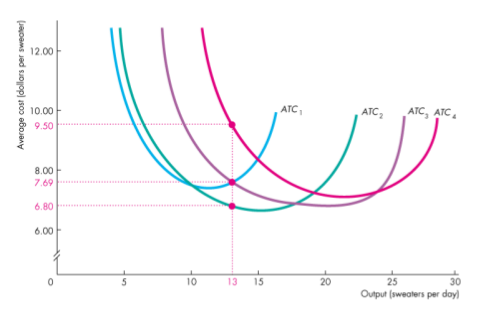

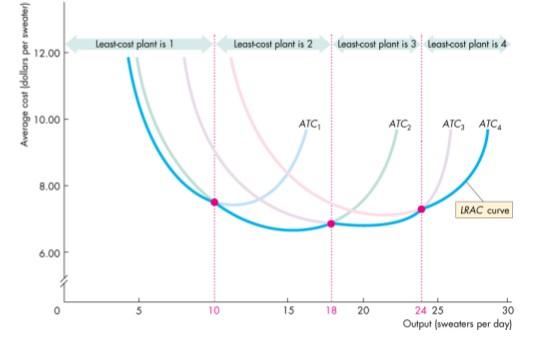

Short and Long-Run Cost

- The larger the plant, the greater it the output at which ATC is at a minimum

- Each plant has a short-run ATC curve

- The firm can compare the ATC for each output at different plants

Long-Run Cost

- Made up from the lowest ATC for each output level

- By comparing the curves using differnet numbers of knit machines, we can see that the least-cost way of producing 13 sweater a day is to use 2 knitting machines ()

Long-run average cost curve - the relationship between the lowest attainable average total cost and output when both the plant and the labour are varied

- A planning curve that tells the firm the plant that minimizes the cost of producing a given output range

Economies and Diseconomies of Scale

Economies of scale - falling long-run average cost as output increases (e.g. technology)

Diseconomies of scale - rising long-run average cost as output increases

Constant returns to scale - constnat long-rn average costs as output increases

Minimum Efficient Scale

- The smallest quantity of output at which the long-run average cost reaches its lowest level

- If the long-run average cost curve is U-shaped, the minimum point identifies the minimum scale output level